WB013: Setting up Rakuten Pay

Rakuten Pay (Japanese: 楽天ペイ) - a cashless payment app - is owned by Rakuten Group, Inc (TYO: 4755), Japan's largest e-commerce company.

The app's payment capabilities are similar to Malaysia's Touch 'n Go eWallet, Singapore's PayNow, China's WePay & AliPay and Japanese competitor PayPay.

I recently downloaded Rakuten Pay to gauge the app's User Experience (UX) as a non-Japanese user. UX is how a user interacts with and experiences a product (hardware or software), and is an important aspect of product development.

I was also motivated me to download the app to boost my Rakuten Point earnings potential.

But first, I needed to top-up my Rakuten Cash (Rakuten's e-wallet) account to settle future Rakuten Pay transactions.

Using snapshots from my mobile phone, I hope to show this user journey, which was successful in spite of my language limitations.

The journey from physical cash to digital cash

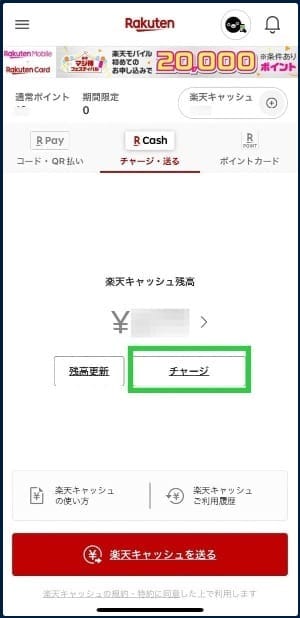

I started by tapping the "チャージ" (English: charge) button (refer to the snapshot below), which I rightly guessed would load the top-up interface. Truth be told, I would not have passed this first step if I did not understand the meaning of チャージ.

The next page listed a number of top-up methods: bank account transfer, ATMs owned by 7-Eleven or Lawson, Rakuma (Japanese: ラクマ), Rakuten Wallet or Rakuten gift cards (Japanese: 楽天ギフトカード).

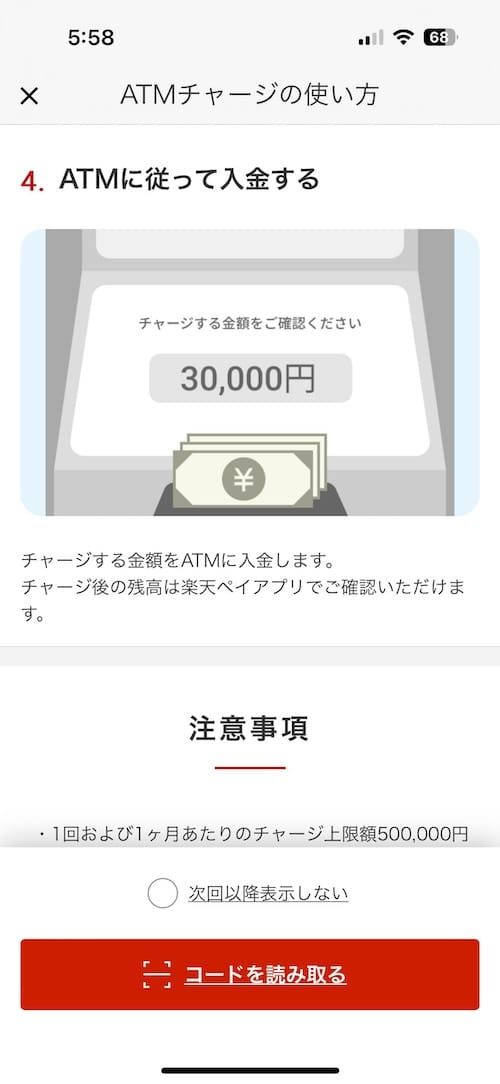

I opted to deposit cash at a 7-Eleven ATM near my home. This turned out to be a fairly smooth experience, and below are the steps I took.

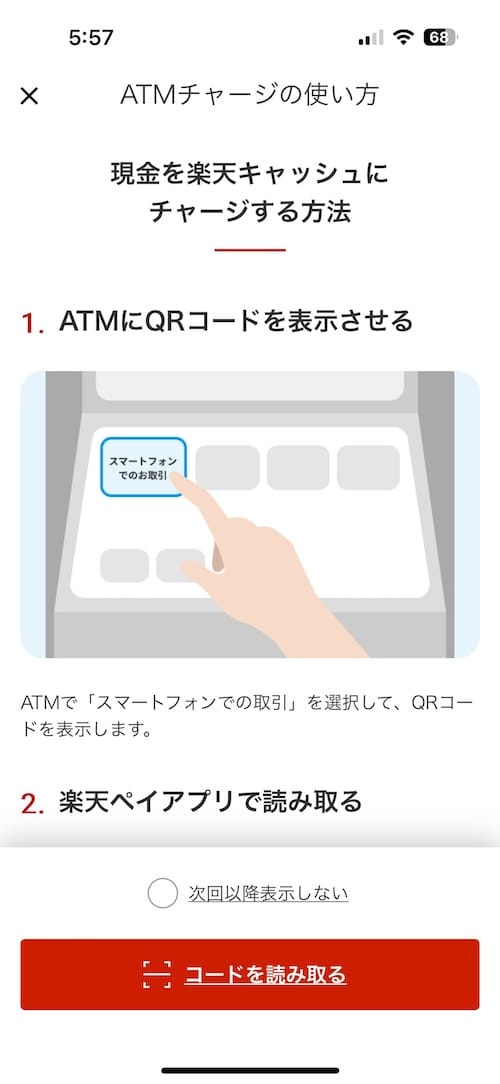

Step 1: I retrieved the ATM's unique QR code.

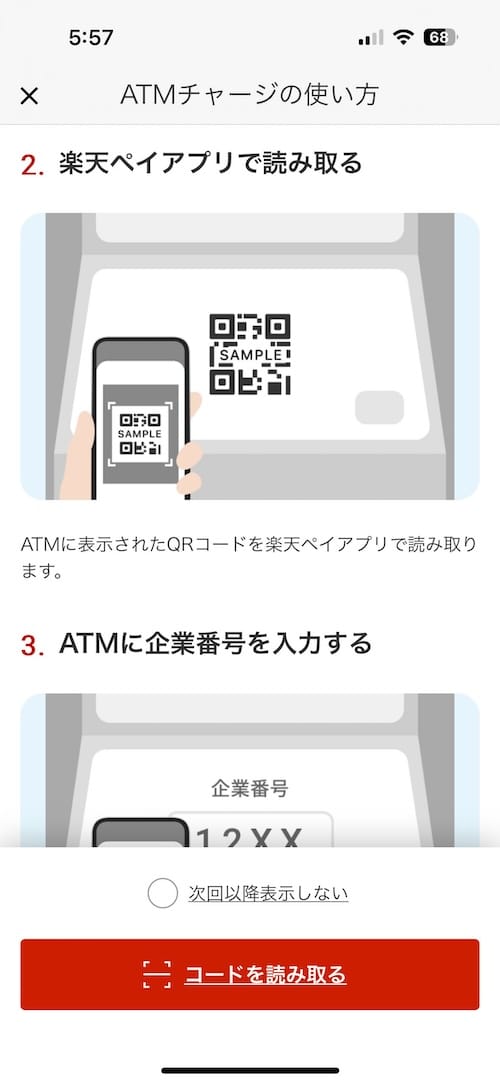

Step 2: I scanned the ATM's QR code with my Rakuten Pay app. This generated a 4-digit code.

Step 3: I entered the 4-digit code into the ATM's keypad, which (I think) authenticated the top-up transaction.

Step 4: I deposited a JPY1,000 note into the ATM and confirmed the total amount. This balance was almost immediately reflected in my Rakuten Cash account.

This ATM top-up method has no fees or charges involved. It is also convenient because 7-Eleven and Lawson have very large distribution networks.

I also repeated the experience at a Lawson ATM, which was just as seamless.

My next experiment will be to complete a payment using Rakuten Pay!

Additional takeaways

I was curious as to why Family Mart, another major Japanese convenience store operator, does not support cash deposits to Rakuten Cash.

I suspect it's because Family Mart does not own a banking arm, while the holding companies of 7-Eleven and Lawson respectively own Seven Bank Ltd (TYO: 8410) and Lawson Bank (privately owned).

I find this interesting as the convenience store operators I know of typically focus on their core operations, offer parcel pick-up & drop-off services and bill payments.

If I were to hazard a guess, I think Seven & i Holdings and Lawson Inc want to leverage their extensive store network to generate ATM fee income (it costs money to withdraw cash from an ATM in Japan).

So long as cash remains relevant, this strategy makes sense.

--Ends