WB017: A Chicken & Egg Problem

Three months after settling into Japan, I decided it was time to open a local bank account and subscribe to a local mobile line. There are several reasons behind this decision, which I will elaborate on in a later article.

To begin my journey, I started looking for a Japanese telco to sign up to. But after some quick research, it appeared most major telcos don't accept foreign-issued cards as a payment method. Opening a bank account - to get a locally-issued bank card - then became my priority.

The Japanese Bankers Association has 114 members. Using this as a yard stick, I had no shortage of banks to pick from. And I was looking forward to deciding based on metrics like best deposit rates, banking app usability and ease of applying.

The illusion of choice

Unfortunately, Japan Post Bank Co., Ltd. ("Japan Post Bank")(Japanese: ゆうちょ銀行)(TYO: 7182) - part of Japan Post Holdings Co., Ltd. (TYO: 6178) - was the only bank I could open an account with.

Reason being, a key requirement for almost all banks is that applicants have established at least 6 months of Japanese residency in addition to having a valid long-term visa. An exception is if you are employed locally.

I think this requirement is in place because banks want to onboard legitimate, long-term customers, especially given the rise in money laundering and financial scams. Prevention is better than the cure, I guess.

Established in 1875, Japan Post Bank has a market capitalisation of JPY4.9 trillion (~USD32 billion) and is one of Japan's oldest banks.

According to its 2024 annual report, Japan Post Bank has a network of 24,000 post offices, deposit base of JPY190 trillion (US$1.25 trillion) and a customer base of ~120 million. The latter equates to nearly one bank account per Japanese citizen, given Japan's population of about 124 million.

Because beggars can't be choosers, I applied for a basic savings account called futsuu kouza (Japanese: 普通口座). The application process was surprisingly foreigner-friendly, with the online form available in English and many other languages.

While applying, I quickly hit a road block because a local phone number was a requirement, likely for two-factor authentication purposes.

A (mostly) happy ending

I now had a chicken & egg type of problem: to get a local phone number, I needed a locally-issued bank card. But to get a locally-issued bank card, I needed a local phone number.

It was back to the drawing board (and Reddit), to figure out how to break this circular dependency. A few hours of research later, I found an Mobile Virtual Network Operator1 ("MVNO") called IIJmio2 that accepts payments from overseas-issued cards.

At long last, I successfully opened my bank account and was relieved at finally getting a debit card.

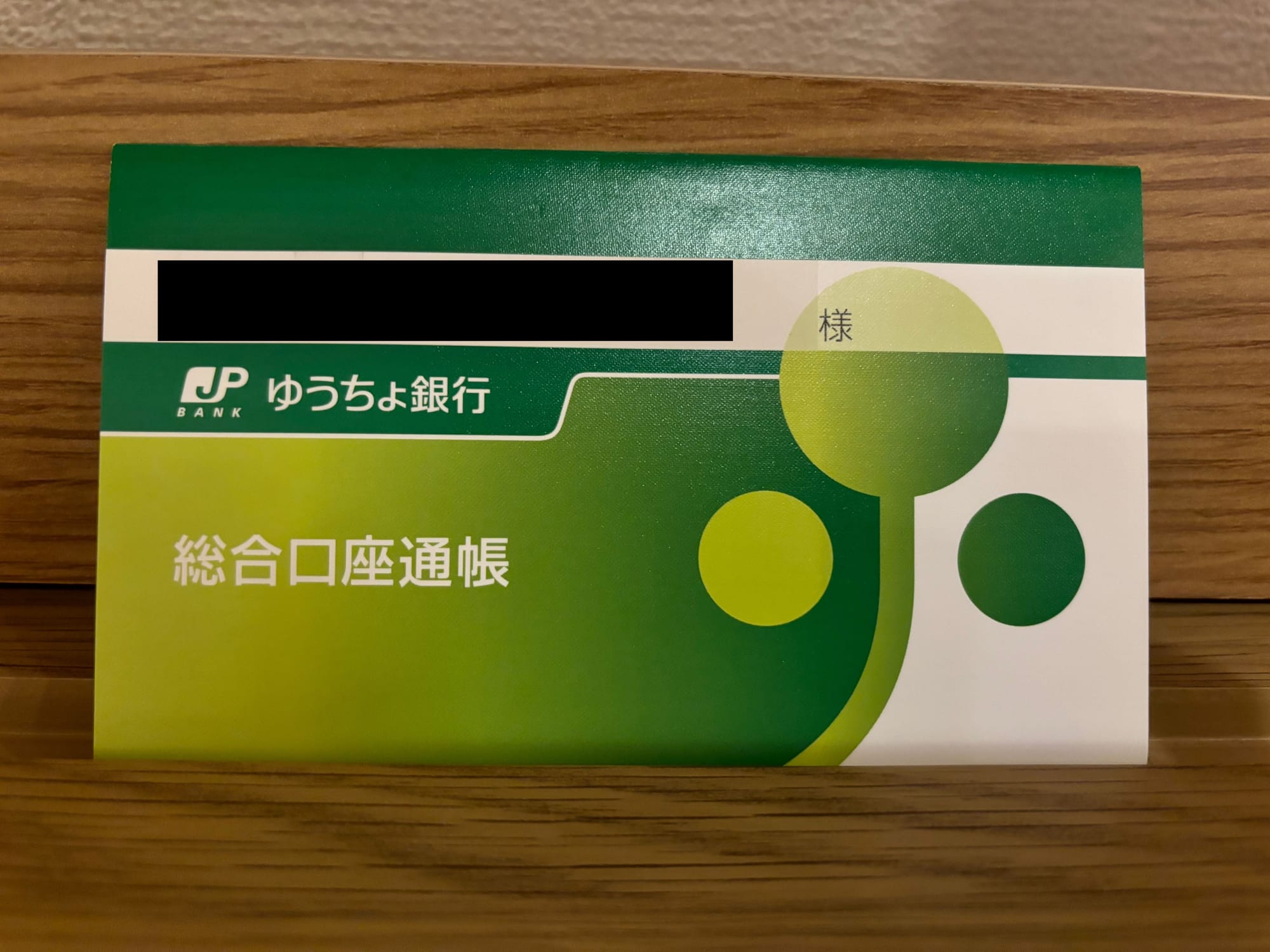

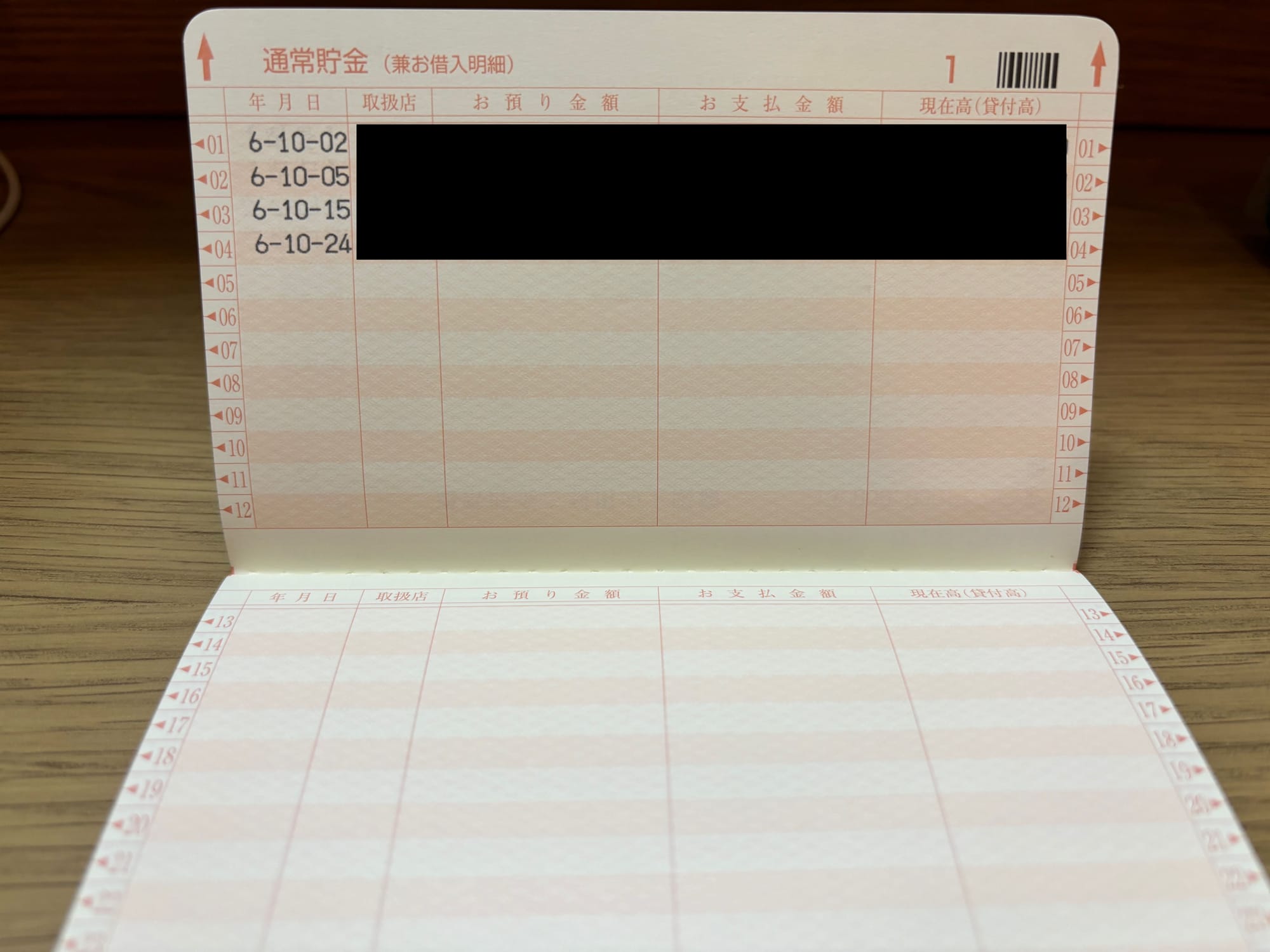

This was not to be the case, however, as the futsuu kouza is only bundled with an ATM / cash card and savings passbook (yes, they still issue passbooks here). In countries like Singapore, Malaysia and Australia, debit cards are now the standard offering given the rise in contactless payments.

Savings passbook (Left, Middle) and ATM / Cash Card (Right)

Slightly disappointed but accepting of the fact that the journey is more important than the destination, I made a separate application online for a debit card.

It was quite a smooth process, though the same can't be said for the outcome: A few days later, I got a letter saying my application for a debit card was rejected. Six possible reasons were offered, with no indication on the specific reason why my application was rejected.

To add further insult to injury, I realised Japan Post Bank's default online banking platform is a view-only portal, i.e. you can only check account balances and transaction history.

To enable transactional banking, you need to download Japan Post Bank's Yucho Authentication App via Apple Japan's App store. Lo and behold, I could not do this because the App store requires a locally-issued debit or credit card.

1 An MVNO does not own the wireless network and instead leverages the network of a major mobile network operator. MVNOs are typically cheaper because they compete with each other (and major telcos) based on price and service offerings. However, MVNOs don't have physical branches unlike major telcos

2 I don't know what IIJmio means.

--Ends