WB018: Why a travel card cannot replace a bank account

If you have travelled overseas for holiday or work, bank-issued credit and debit cards are used as a last resort because of hidden fees and poor exchange rates. Carrying wads of foreign currency remains the default means of payment for many travellers.

Fortunately, things are rapidly evolving in the travel card space as technological and product innovation has increased competition and driven down costs to consumers.

Case in point is the rise in popularity of travel payment-focused financial technology companies ("fintechs") like Wise PLC ("Wise")(LON: WISE) - yes, it's been listed since 2021 - and Revolut.

Interestingly, Wise's market capitalisation of GBP8.4 billion (~US$10.8 billion) exceeds that of The Western Union Co (NYSE: WU) - the 150-year old "OG"1 of cross-border transfers - by nearly three times.

How stagnant the once mighty have stayed.

I have recently been experimenting substituting a Japanese bank account with a Wise card and Singapore-issued travel debit card. These products have, for the better part, fulfilled my daily transactional needs.

Why I need a Japanese bank account

Three months in, and I decided it was finally time to open a local Japanese bank account due to a combination of factors.

Firstly, for Japanese tax reasons I need to track the total amount of foreign-sourced income remitted to Japan. Using a travel card (or any card for that matter) to make payments in Japan counts as a remittance.

It is easier from an administrative point of view to remit one budgeted lump sum to a Japanese bank account. By using a travel card, I'd have to go through monthly bank statements and identify all relevant travel card transactions.

Secondly, ATM fees are incurred each time I withdraw cash from my travel card in Japan, where cash is here to stay. Each ATM withdrawal is also capped at JPY100,000. This is sufficient for mandatory spending - groceries, meals, transport etc - but not ideal for bigger ticket items like rental expenses and emergencies.

I am also mindful that the Singapore bank issuing my travel card may be more inclined to block regular cash withdrawals from overseas sources. I therefore feel safer withdrawing cash from a local bank account.

The final reason relates to restrictions imposed on travel cards issued by Fintechs.

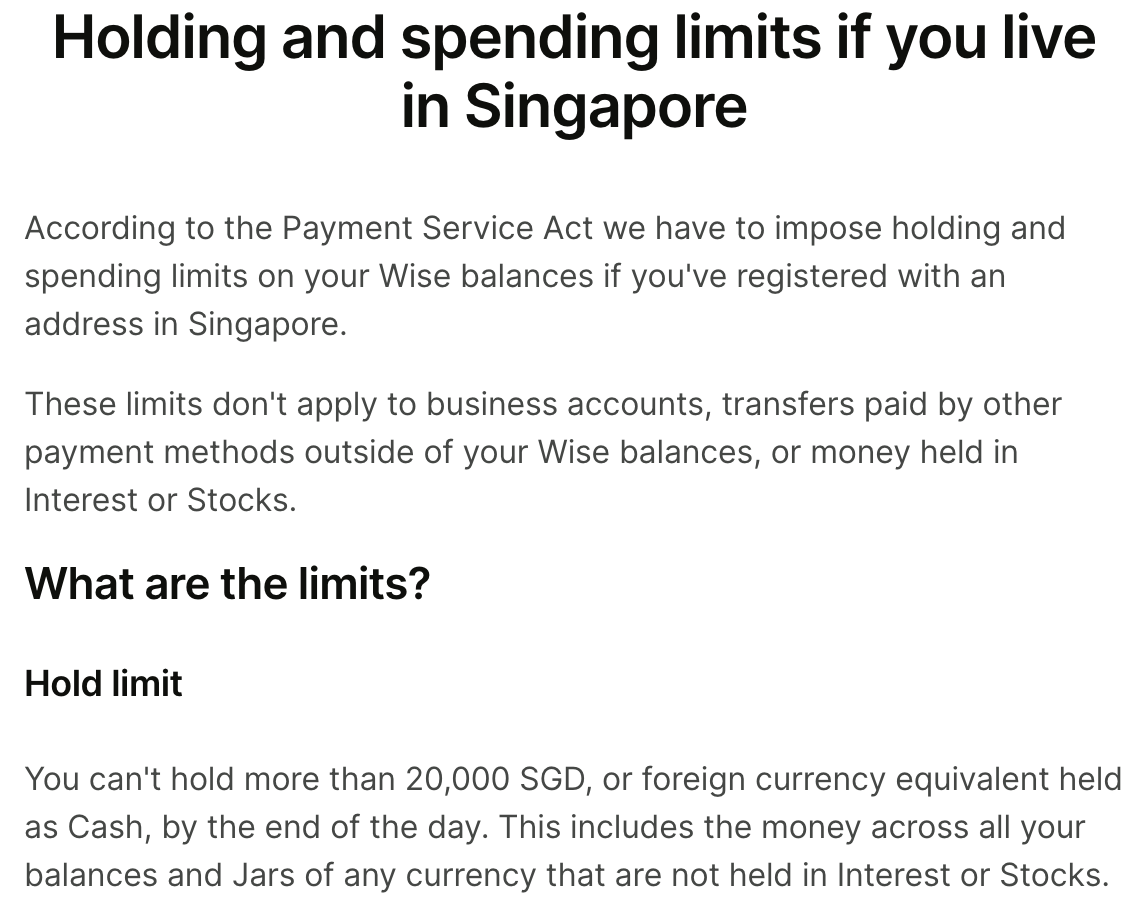

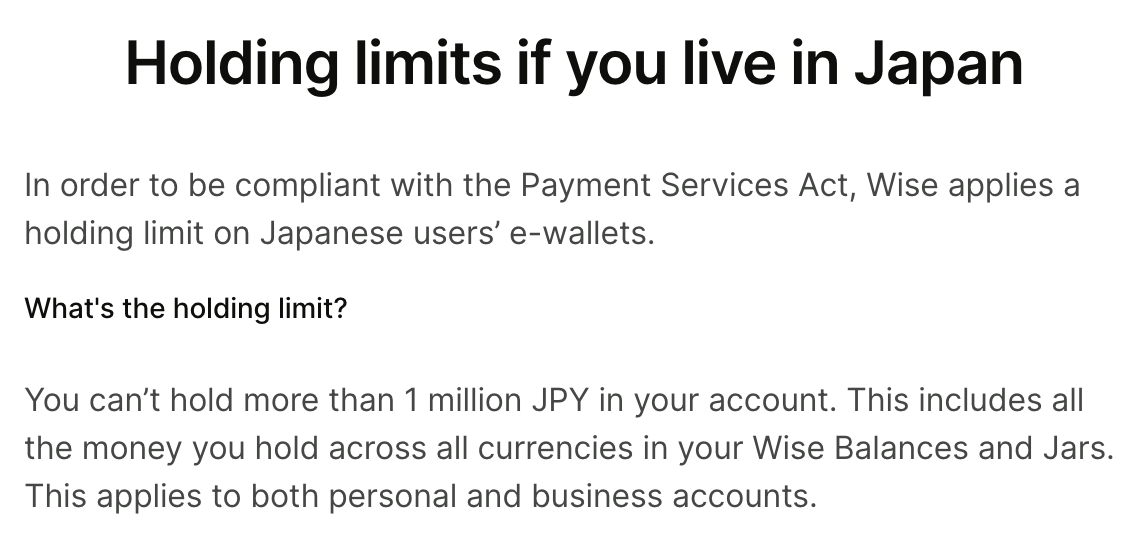

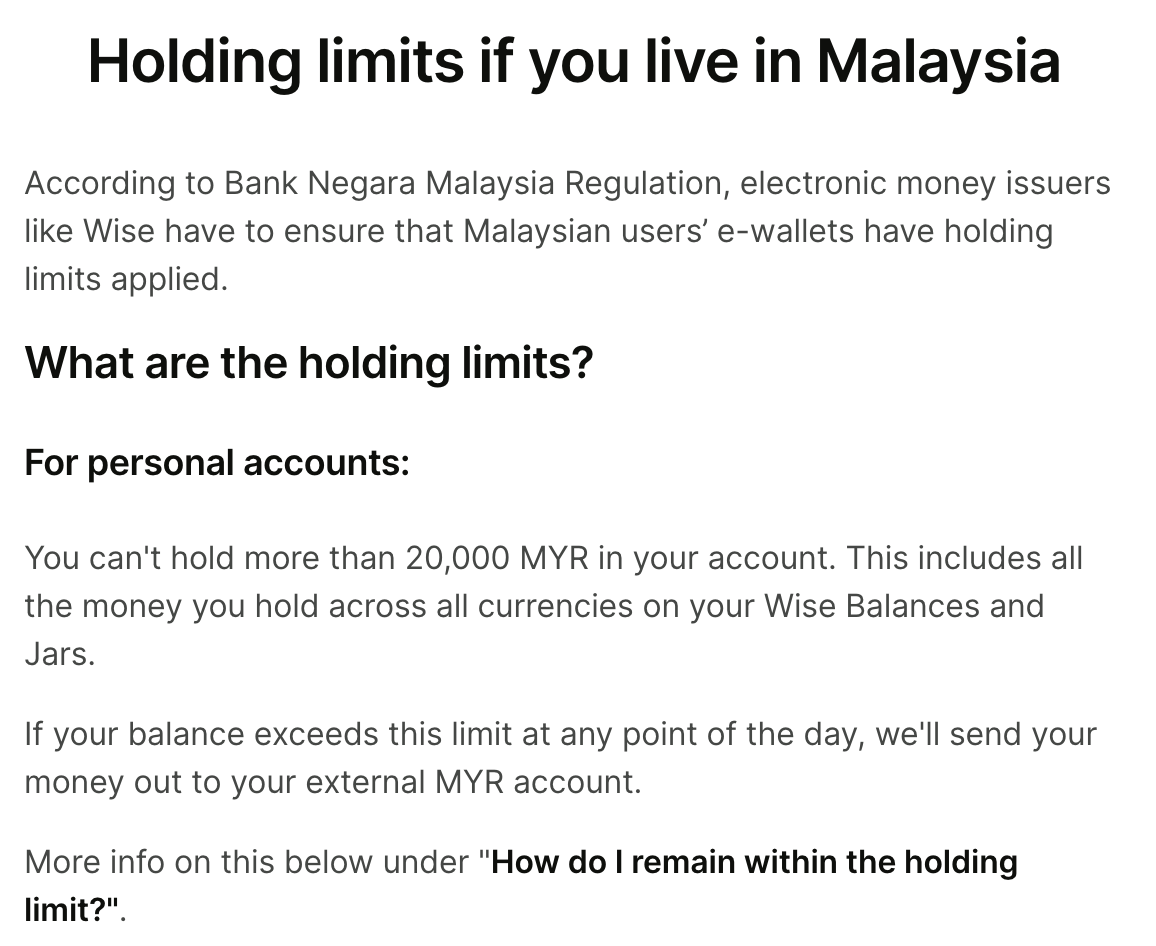

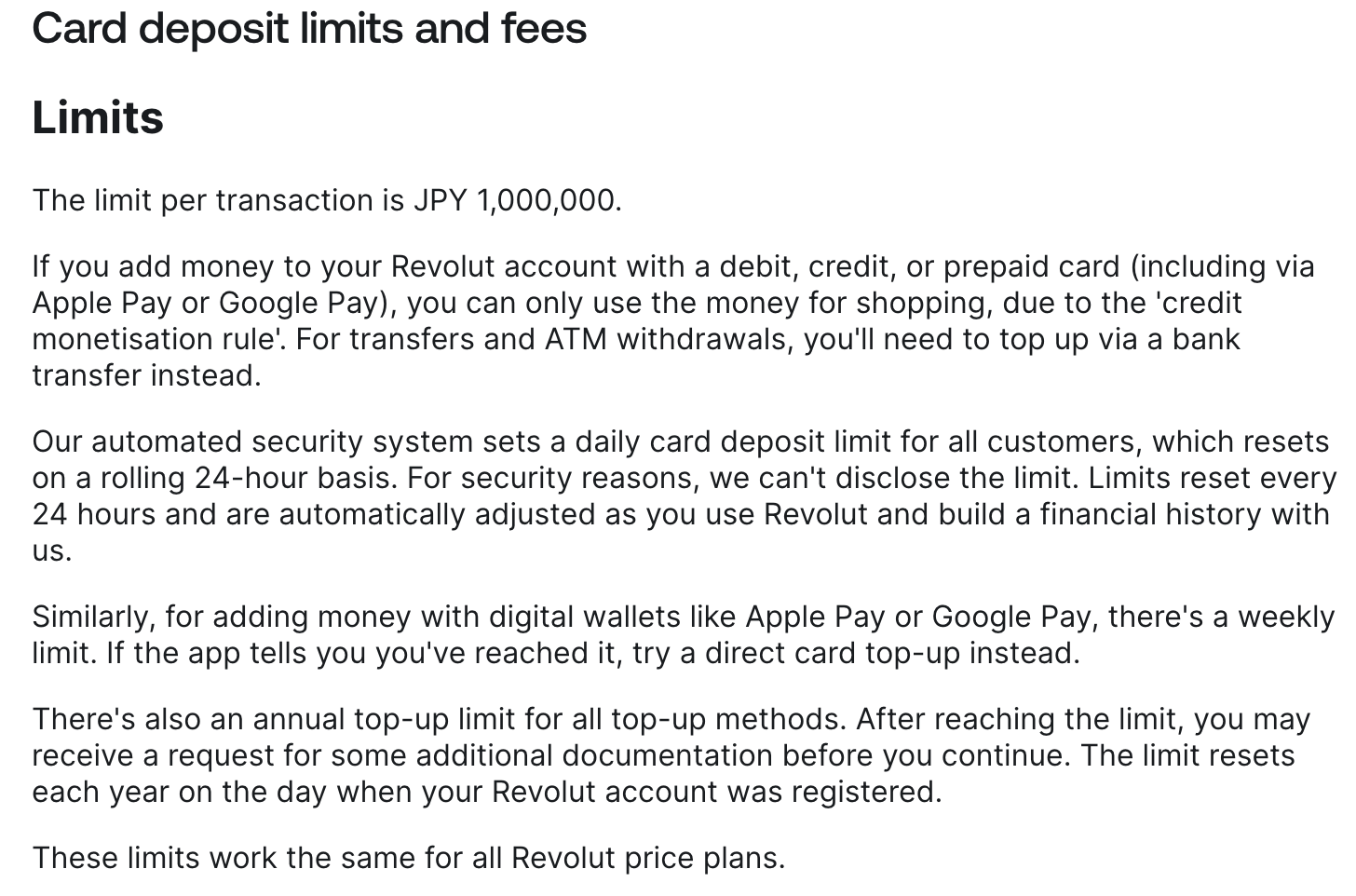

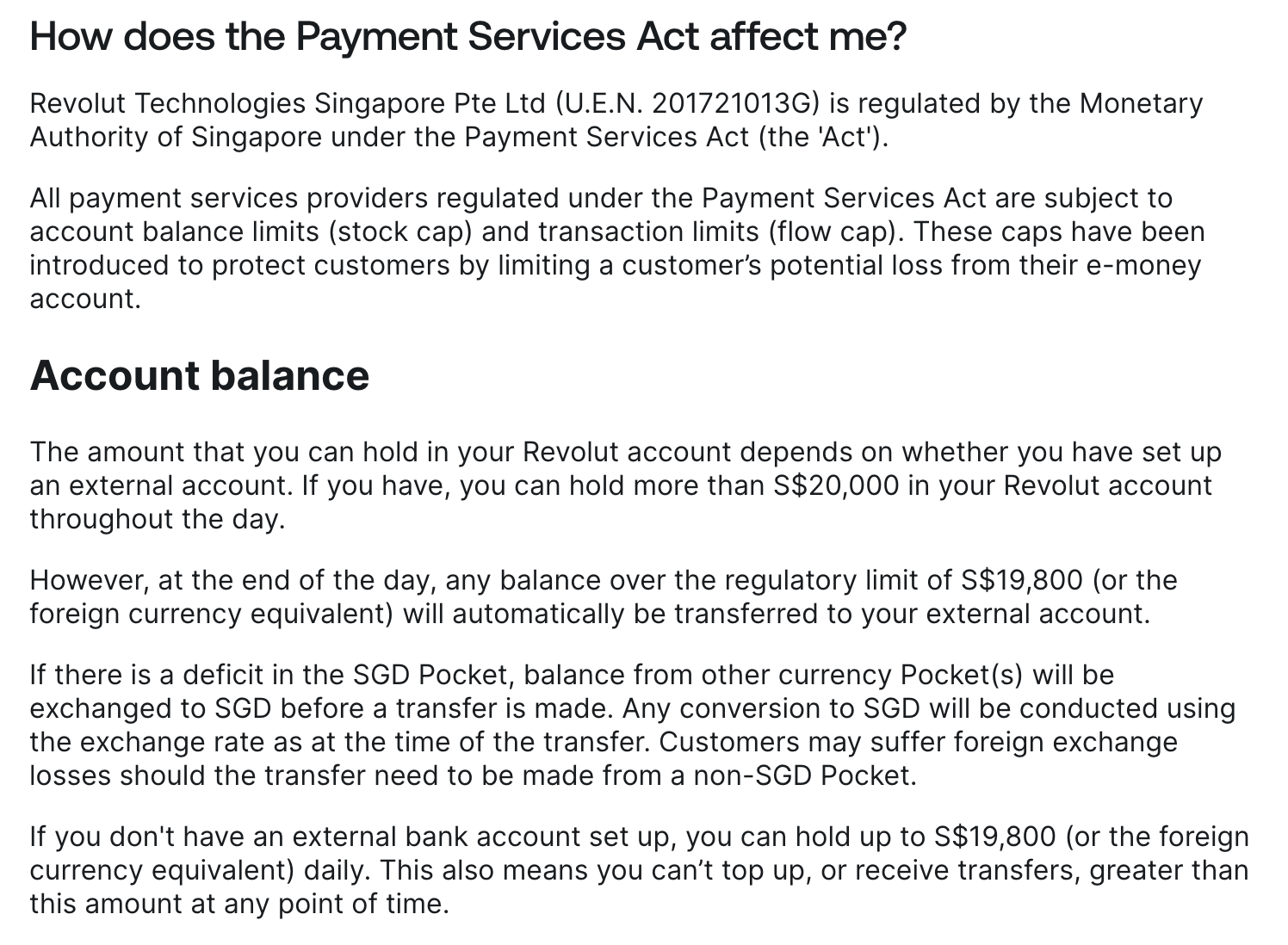

Because of local financial regulations, Fintechs have annual holdings limits that vary from country to country. In Japan, Wise users have an annual holding limit of JPY1 million (~US$6,500). In Malaysia, it is RM20,000 (~US$4,600). In Singapore, it is S$20,000 (~US$15,100)

Don't get me wrong, for travel purposes these limits are more than sufficient. But if you plan to start building some savings, you're better of with a traditional bank account.

Wise's country-specific annual holding limits

Revolut's country-specific limits

Despite the reasons above, I think it's still worthwhile retaining a travel card for short-term travels. It is also important to continue using new products to be in touch with the latest innovations.

A Wise investment?

Prior to writing this article, I had no idea Wise was listed on the London Stock Exchange. As it turns out, the company was listed via a direct listing in 2021. A direct listing is done without intermediaries like investment banks, unlike an initial public offering.

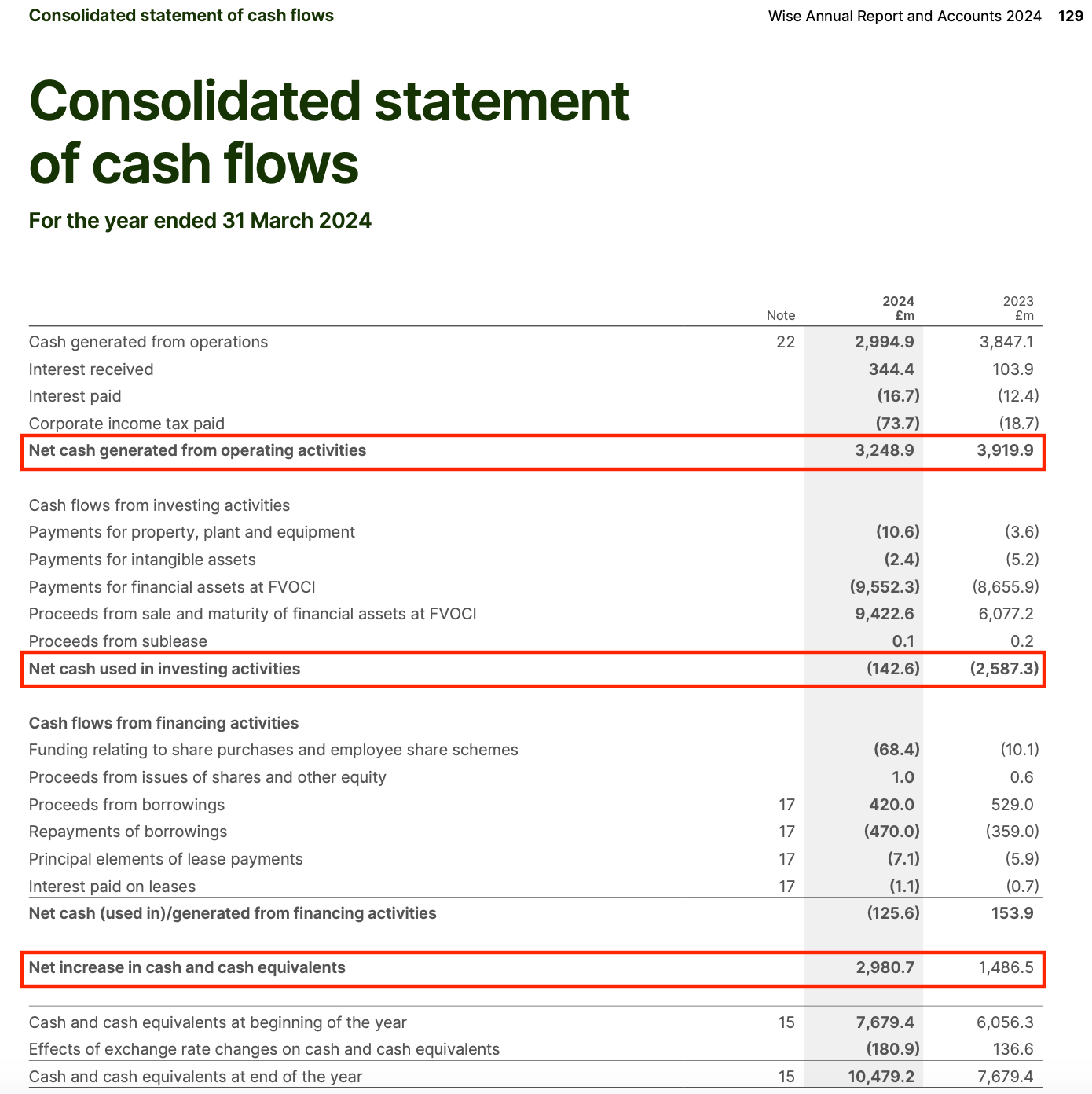

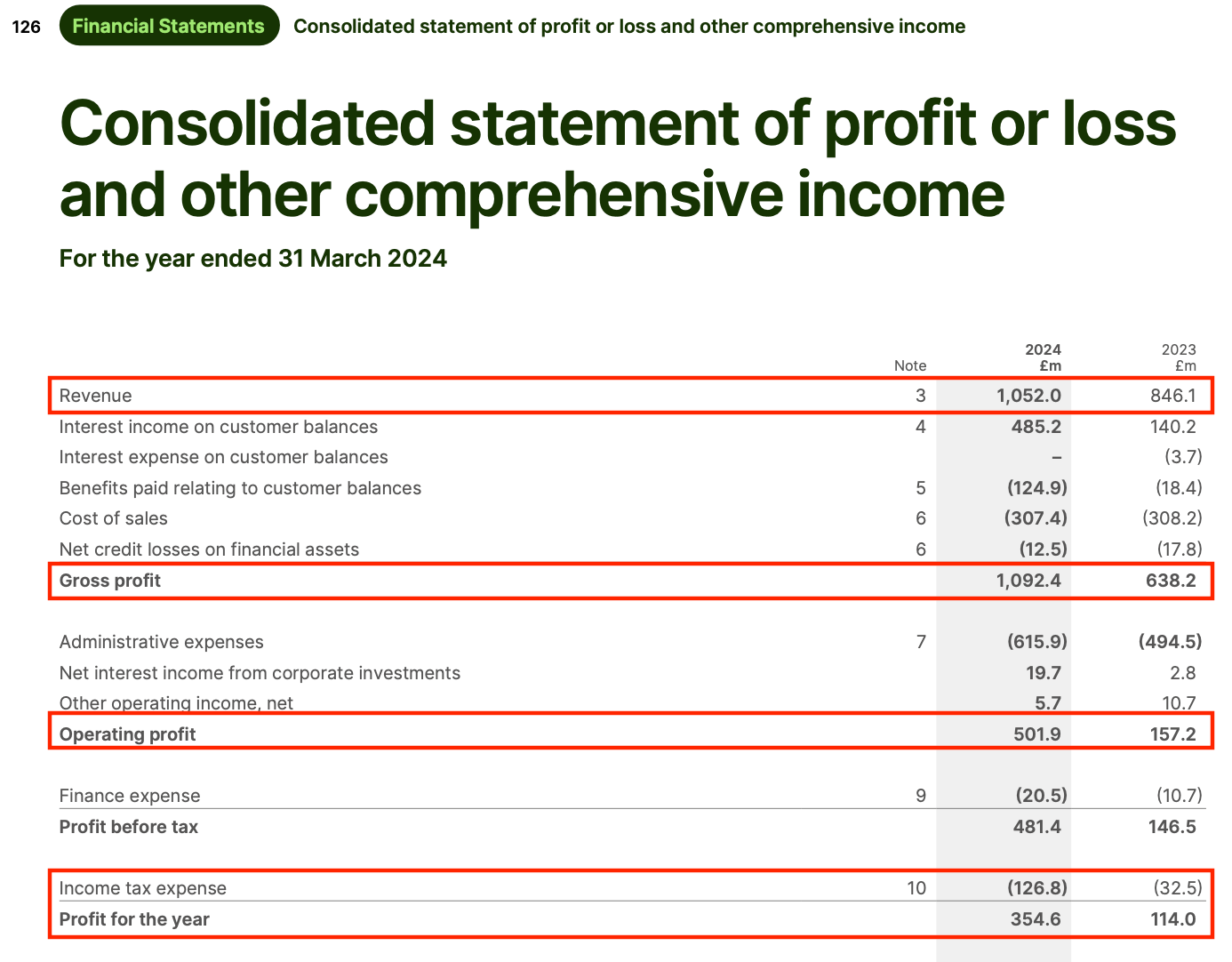

Wise's shares have not performed terribly well since its IPO, but what's important is that it's profitable (cashflow-wise) and growing at a nice clip. Most tech companies are growing, albeit unprofitably.

A cashflow positive, profitable tech company

As a user of Wise, I must say the company's market valuation reflects the great product the company has built over the years. This has helped the company grab market share from the incumbents players who have been slow (or comfortably unwilling) to innovate.

Peter Lynch, a famous value investor who very successfully ran Fidelity's Magellan Fund, strongly believes individual investors can achieve superior returns by investing in what they know.

If you are a Wise user, you should spend time taking a closer look at Wise's publicly-available financials to see if you can ride on its success.

1"OG" is the acronym for "Original Gangster", a term coined describe (according to Merriam-Webster) "someone or something that is an original or originator and especially one that is highly respected or regarded".

--Ends